General information

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

8 (800) 700 95 53

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

Insurance services can be divided into several types, taking into account various characteristics.

Depending on the risks, there are the following types of home insurance:

- personal property;

- type of liability to third parties.

Insurance contracts specify a mandatory list of housing elements, in case of damage to which the insurance company will be held liable. These may include household goods, interior decoration, etc.

If the contract provides for liability measures to third parties, then the insurance company will have to compensate them for damage if for some reason their property is damaged.

Some insurers offer their clients to enter into an agreement that provides for various risks of property damage, as well as damage from third parties.

Objects

The main objects of insurance include real estate (apartments, mortgaged housing, private houses). Each of the objects has its own nuances, which should be paid attention not only by policyholders, but also by insurers.

Apartment

This type of apartment insurance is relevant for old buildings where worn-out communications are installed. This property is most often exposed to various risks.

You should not overlook the insurance of apartments located in new buildings. Home insurance is especially relevant after expensive repairs.

If desired, you can take out civil liability insurance. This approach will allow you to insure liability to neighbors in a residential building.

A private house

Insurance of private houses does not have any special distinguishing features from apartment insurance, but there are still certain nuances:

- it is necessary to take into account not only the house itself, but also the buildings located next to it (bathhouse, garage, etc.);

- for the insurance procedure, you will need to collect the necessary papers, taking into account a number of details;

- You can also insure an unfinished house that you own and is at the stage of completion of construction.

Private houses are usually insured against fires. The presence of a fire alarm, bars on the windows of the house, high-quality materials for construction and finishing insurance will help you save on insurance. Insuring a house built from timber will be cheaper than insuring a residential house built from brick.

Policy cost

An insurance contract for a residential building (or cottage) can be concluded either with its assessment by a representative of the insurer, or without it (with the presentation of property documents and photographs to the insurance company).

Without an appraisal, houses that are standard for a given region are insured at their average market value. The insurance premium (your payment) is calculated as a percentage of the total value of the property. Usually this is 0.2-0.3%.

If you classify your property as elite and value it above the regional average, you should call an insurer for an objective assessment.

But remember, no matter how much you value your home, your insurance compensation cannot be higher than the actual cost of rebuilding the home (even if you enter into a contract for a large amount).

When calculating your compensation for the restoration of the lost part of the property, the insurance company will proceed from the current price of building materials in the region plus payment for the necessary restoration work. In total, this can be significantly less than the market value of real estate in the region, which consists of the market situation, the location of the house, and its prestige.

What affects the price?

Your insurance will be more expensive if:

- you have a wooden house;

- Your house is heated by stoves and has a wood fireplace;

- your property is located in a potentially dangerous area;

- your property is located in an unguarded area;

- you rent out a house or cottage;

- if your housing is temporary, for example, seasonal;

- if you have previously had insured events;

- your dacha is not equipped with bars on the windows, an iron door, an alarm system, or video surveillance;

- you have included the maximum number of risks in the contract;

- you will pay the insurance premium in installments.

Each of the points increases the cost of insuring houses and summer cottages slightly. However, when several factors are added together, the insurance premium can increase significantly.

How to reduce your insurance premium?

Protect your home yourself: install metal doors; put bars on the windows (and basement); equip your house with an alarm system; area - video surveillance.

Choose a proven, large insurance company and cooperate with it on an ongoing basis. Renewing the contract without any previous insured events significantly reduces your payment.

If the installment plan includes interest, pay the insurance premium in one lump sum.

Negotiate a reasonable deductible - those damages or losses that you are willing to restore at your own expense. For example, broken glass at the dacha or petty theft at the site. This step is welcomed by insurers and leads to a reduction in the percentage of insurance premiums.

Remember that if an insured event occurs, the company will only reimburse the cost of lost property. This means that if the house burns down and its foundation is not damaged, it will not be paid for.

When concluding a contract, you should minimize the cost of parts of the house (as a percentage) that will survive the force majeure you have agreed upon.

Law

Real estate insurance is regulated by a number of legislative acts:

- Federal Law No. 102 “On Mortgage”, when it comes to mortgaged housing (Articles 29, 31, 32).

- Federal Law No. 4015-1 “On the organization of insurance business” - contains the procedure for regulating legal relations between the insurer and the policyholder.

- Civil Code of the Russian Federation - articles 929-930, 940, 943.

Home insurance

Residential property insurance is one of the effective ways to reduce the risks that may occur as a result of damage or loss of real estate. No one can predict in advance the occurrence of emergency situations, which include fire, floods and other troubles associated with damage or loss of housing.

Home insurance, which has distinctive features depending on the type and condition, will help reduce risks and costs.

Voluntary

Insurance is a voluntary procedure, therefore, the owners of residential premises themselves have the right to decide whether to purchase an insurance policy or not. When choosing an insurance package, you should take into account the expected risks and available financial capabilities.

The most profitable options are package offers, which provide for the possibility of including various situations in insurance cases that could lead to losses.

Read about receiving subsidies for young families to purchase housing. How does the program to provide housing for young families work? See here.

With a mortgage

Taking out mortgage insurance is mandatory. Using this method, lenders try to minimize possible risks in case something happens to the home and the mortgage loan still has to be repaid.

You should not regard home insurance for a mortgage as an additional expense. In practice, lenders approve applications without insurance at a fairly high interest rate, which is not beneficial for the borrower.

No one can guarantee that nothing will happen to the property or the borrower during the term of the mortgage agreement.

From fire and flooding

It is necessary to understand that the policyholder will interpret any controversial issues in the event of flooding or fire in the home in favor of its interests. Before signing a contract, you need to be aware of what your home may suffer as a result of a fire.

There are three options here:

- from exposure to direct fire;

- there was interaction with combustion products;

- the fire occurred as a result of the actions of third parties when extinguishing the fire.

The wording and mention of these three options when concluding a contract is very important. It is they who will determine what compensation a citizen is entitled to.

As for flooding, the neighbors through whose fault the incident occurred are required to pay for the losses incurred. But what to do if there is no one to demand compensation for losses from? In this case, an insurance contract will come to the rescue, providing for conditions for compensation, even if the owner of the apartment himself is to blame for the incident. For example, a pipe burst in a house and flooded the neighbors. It will not be the homeowner himself who will compensate them for their losses, but the insurance company.

It is important to correctly spell out the terms of the contract, taking into account any details and subtleties.

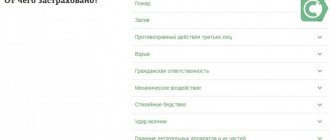

How to choose risks?

Each owner is free to independently choose what he wants to insure his house or cottage against (the price of the policy will depend on this). The standard contract provides the following options:

- From a fire that occurred as a result of an accident (arson - separately).

- From domestic accidents - gas explosion, damage to plumbing or heating.

- From fire, lightning, natural disasters. Natural disasters may include earthquakes, hurricanes, tsunamis, mudflows, landslides, hail, and heavy rains. Here you should soberly assess the possibility of their occurrence if your home is located, for example, in central Russia.

- From criminal actions of third parties - arson, theft, burglary, destruction of property, vandalism.

- From falling objects from above (trees, airplanes) or being hit by vehicles.

No insurer will include in the policy the risks of property loss that occurred as a result of:

- exposure to radiation;

- military actions;

- riots, pogroms.

All points should be carefully studied, their feasibility assessed, the necessary ones selected, and only then an agreement should be concluded.

Programs and tariffs

Insurance programs are presented in the form of classic products that provide individual sets of risks for each object. Typical real estate is insured with “out-of-the-box” programs, which already define the conditions, amounts and risks.

Why such programs are convenient:

- relatively low cost;

- fixed amounts of compensation are determined in advance;

- there is no need to describe the property in advance;

- Insurance can be purchased online on the insurer's website.

Classic programs are less in demand. Their advantage lies in improved service and wider risk coverage.

The cost of the policy is calculated individually and depends on the number of included objects of insurance.

Sberbank offer

Sberbank offers various types of property insurance policies. If any option occurs, the injured subject will receive monetary compensation if his home or property is damaged as a result of the occurrence of an insured event provided for in the contract.

Insurance programs are divided into:

- mandatory – regarding mortgage housing;

- voluntary – at the choice of the property owner.

Currently, the bank operates three insurance programs:

- from fire and flooding;

- "protection" of the house;

- insurance of land against flooding.

Types of insurance policies for real estate

The Russian insurance market offers to insure residential buildings, suburban areas and cottages against fire and other risks, using various programs to choose from.

Article on the topic: Features of real estate insurance in Sberbank Insurance

The following types of insurance for country houses are distinguished:

- Title. The program is relevant for property owners who have purchased property, but are afraid that in the future the completed transaction will be considered illegal for one reason or another (presence of encumbrance, errors in documentation, etc.).

- Mortgage. A must-have product from lending institutions. If you do not insure your mortgaged home against fire and other risks, the bank will not issue a loan.

- From loss of property. Insurers will refuse to issue such insurance if the structure is recognized as unsafe or is frankly dilapidated. The policy provides owners with protection against destruction of the building associated with poor-quality construction and repair work, and cheap metal structures used.

- Civil liability. If the policyholder unintentionally causes damage to third parties through his actions (for example, by flooding them), the insurance company will pay compensation to the victims.

- During repairs. If major renovation work is being carried out on a house, then you can insure the structure (the entire building, the property located in it), and individual structural elements. Also, insurance is often issued for new engineering equipment and finishing that appeared after repair work.

Important! Unregistered houses and buildings cannot be insured. This is a legal requirement. Large insurance organizations will not consider such proposals from potential clients.

Registration procedure

Registration of a policy implies the following actions:

- determination of possible risks against which housing will be insured;

- choosing the optimal type of insurance;

- determining the insurance company where the policy will be issued;

- collecting the required package of papers;

- studying the terms of the contract by both parties to the transaction;

- signing the main agreement;

- payment by the citizen is required amount.

Conclusion of an agreement

The signed agreement comes into force on the day following the day the insurance premium is paid.

The contract must include:

- information about the parties, indicating their data and details;

- list of insured property and insured events;

- the amount of the insured amount;

- procedure for payment of insurance compensation;

- cases when payments are not due;

- liability of the parties;

- contract time.

All terms of the contract must not contradict the law. Interested parties carefully read the terms and conditions before signing the papers, paying special attention to insured events.

Required documents

From the papers you will need to prepare:

- passport;

- confirmation of ownership rights to the insured property;

- technical plan from BTI;

- real estate valuation report.

These papers are considered basic. Different insurance companies have the right to require different documentation.

A sample property insurance contract is here.

How to get home insurance?

The insured can be: the owner, members of his family, persons renting the house. The rules for insuring property of individuals are established by the laws of the Russian Federation and insurers. They are usually different for individuals and legal entities.

They contain the following points:

- general provisions;

- duration of insurance;

- cost of issuing a policy;

- list of available risks;

- list of conditions for payment of compensation;

- possible objects of fire insurance;

- explanations of the terminology used;

- the procedure for establishing the value of real estate, the extent of damage caused, and monetary compensation;

- procedure for transferring compensation to the policyholder's account;

- settlement of disputes.

Selecting an insurance agency and insurance policy package

Insurance companies offer personal property insurance conditions for individuals. The following objects can be insured:

- rooms, premises;

- unfinished construction projects;

- cottages, country and private houses, dachas, outbuildings;

- capital construction projects.

Article on the topic: Features of a security deposit when renting an apartment

Exceptions from insurance coverage - any events that, based on their basic properties and characteristics, are an insured event, but their consequences are not covered. Such exceptions include: military actions, attempts by the policyholder to commit illegal acts, damage to the insured property while under the influence of alcohol or drugs, etc.

Large insurance organizations in Russia offer the following conditions for insuring houses against fire and other risks:

- "Rosgosstrakh". The offered programs allow you to insure various objects: country houses, outbuildings, dachas, including those that were built according to exclusive designs and built using special building materials.

- SOGAZ. The company offers mutually beneficial conditions for insuring objects against fires, floods, natural disasters, and illegal actions of third parties.

- Ingosstrakh. In addition to the main object, the policyholder also has the opportunity to additionally insure individual structural elements of the building, engineering equipment, finishing, movable property, and civil liability.

- Sberbank Insurance. You can choose the appropriate insurance amount, the monthly percentage of its payment, and save up to 10% of the policy cost by paying. Sberbank pays monetary compensation of up to 100,000 rubles without providing certificates.

- "Alpha Insurance" You can insure: houses of permanent and seasonal residence, townhouses, cottages, various buildings (located on the owner’s territory), movable property, valuables, civil liability to third parties.

It's difficult to say where is the best place to insure your home. But you need to choose a large and trusted company that offers a large number of programs and insurance products to choose from and has many reviews on the Internet.

Calling an appraiser from the insurance company

Before signing a contract with the insurer, it is necessary for an expert to come to the insured object, inspect it, and check everything that is required. It is this specialist who will draw up an act (in accordance with the Federal Law “On Valuation Activities in the Russian Federation”), and will also give recommendations to the insurance company regarding the final cost of insurance and whether it is worth working with the client at all.

Collection of necessary documents

The list of required documentation is as follows:

- civil passport of the Russian Federation;

- papers that confirm ownership of real estate (or the presence of a property interest);

- application addressed to the director of the insurance company (sample).

Signing the contract

An agreement with specified insured events, terms, risks (fire, flood, theft, destruction of an object, etc.), rights and obligations of the parties and other points is signed at the insurer’s office after an assessment of the property and study of the act drawn up by an expert.

If we talk about how to properly insure a house, it is worth noting that you must definitely study the contract you sign - it is important that the agreed conditions fully comply with those specified in the agreement.

For how long?

Most often, housing is insured for a period of one calendar year. Some people issue poles for the period during which the owner will not be in the home. For example, during vacation. Short-term insurance is not profitable, so it is advisable to take out a policy for a long period.

Find out where to start buying a resale apartment. What are the bank interest rates on mortgages for secondary housing? Information here.

How to get a loan for secondary housing? Details in this article.

Price

The exact cost of the insurance policy will depend on various factors:

- number of insured events;

- expiration date of the plisa;

- maximum payment amounts;

- cost of the insurance object;

- condition of housing;

- interest rate when it comes to mortgage insurance.

The size of the policy is calculated individually in each case.

Home insurance is primarily issued in the interests of the owner. It is he who must decide on the objects that will be insured and the choice of the insurance company. If the choice is made, when concluding a transaction, you must carefully read the terms of the contract, paying attention to all the nuances and pitfalls.